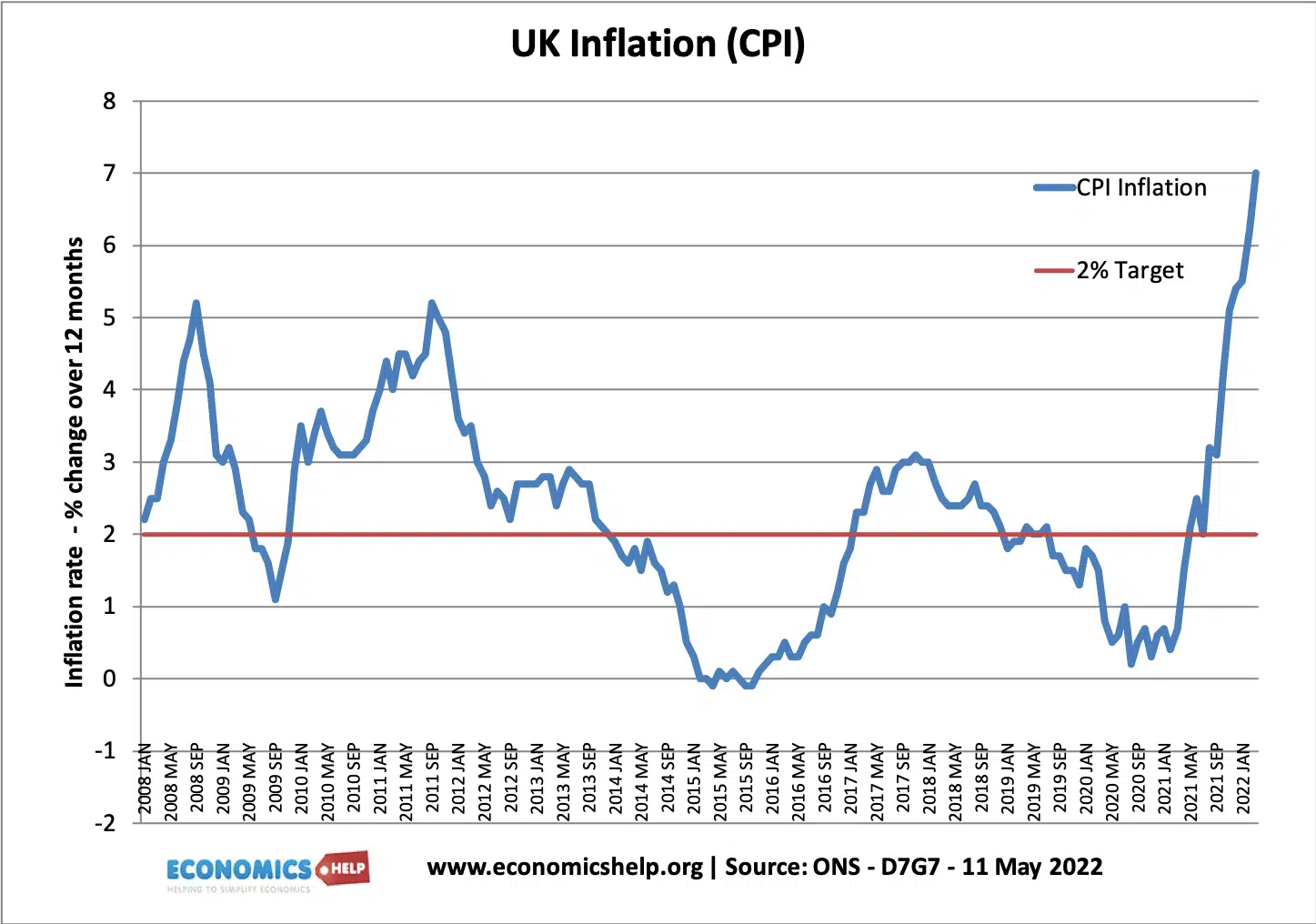

Are you among the one million UK households facing the end of your fixed-rate mortgage? With interest rates soaring, the Bank of England warns that many homeowners could see their monthly repayments jump by £500 or more in the coming years. But fear not! Our financial advisor, Chris Ridge, from My Financial Pro, is here to guide you through six essential steps to prepare for this transition and secure your financial future.

- Speak to Your Lender:

As the end of your fixed-rate mortgage approaches, don't hesitate to reach out to your lender. With the recent increase in mortgage rates, many lenders now offer support measures to help homeowners facing higher payments. You might be eligible for a temporary switch to an interest-only mortgage for up to six months, without impacting your credit score. Additionally, lenders have agreed to delay repossession proceedings for borrowers facing long-term financial challenges.

- Check Your Mortgage End Date:

The first step is to know exactly when your current fixed-rate mortgage deal is set to end. Review your mortgage contract to determine the remaining term. If you take no action, you will automatically be moved to your lender's standard variable rate. Understanding your current monthly payments and the outstanding balance will help you plan and budget for the future effectively.

- Lock in a New Mortgage Rate Early:

Consider securing a new mortgage rate three to six months before your current deal ends. By doing so, you protect yourself from potential rate increases. Some lenders may even allow you to cancel your fixed-rate deal without penalties if rates drop before the new one starts. Chris Ridge recommends checking with your lender about their flexibility in case rates change after you've accepted the offer.

- Consult a Mortgage Broker:

Navigating the mortgage market can be overwhelming, especially when faced with rising rates. That's where a mortgage broker comes in handy. Chris Ridge, the expert advisor at My Financial Pro, advises seeking his guidance. We have access to exclusive deals and can tailor their advice to your specific needs. We can also explore product transfers with your current lender, which might save you money.

- Budget for Increased Repayments:

As your new deal approaches, it's crucial to prepare for higher mortgage repayments. Calculate how much your mortgage will increase by when the new deal starts. For some, this might involve adjusting spending habits or finding ways to boost income. Chris Ridge recommends creating a strict budget and exploring ways to increase your earnings to navigate these changes smoothly.

- Consider Overpaying Your Mortgage:

If you're fortunate to have a low-interest rate, Chris Ridge suggests considering overpaying your current mortgage, if possible. By doing this, you can reduce your outstanding balance and minimise the amount of interest you'll pay on your next deal. Keep in mind that most lenders allow penalty-free overpayments of up to 10% of the remaining balance each year.

Remember, proactive planning and seeking expert advice can make a significant difference in securing your financial future. Chris Ridge and the team at My Financial Pro are dedicated to helping you navigate these changes with confidence. For more helpful tips and personalised guidance on home finance, follow us for future updates and get in touch with My Financial Pro today.